@Alco Hauler Pretty much what I was trying to tell you about AOBC, but I suck in explaining the why I analyze.

Summary

Strategy shift to focus on expanding into non-cyclical markets.

Management is making wise capital allocation decisions with high ROIC.

Based on ROIIC and capital reinvestment rates, AOBC is growing the intrinsic value of the business by 24% annually.

Overview

American Outdoor Brands, Corp. (NASDAQ:

AOBC), formerly Smith & Wesson Holding Corp. (SWHC), is a holding company that markets firearms and outdoor sporting goods under various brands such as the Smith & Wesson, Crimson Trace, and Battenfeld Technologies, among others. The company's history stretches back over 160 years where they got their start manufacturing firearms under the Smith & Wesson brand. For those that are unfamiliar with the Smith & Wesson brand, I would consider it the Nike or Coca-Cola of the firearms industry where one out of every two revolvers in the U.S. today is a Smith & Wesson. Many Americans are familiar with the S&W brand through ownership of a firearm, association with S&W owners, or S&W media exposure in such movies as "Dirty Harry." Today, the S&W brand is housed under the AOBC umbrella, is the one of the leading manufacturers, marketers, and exporters of firearms in the U.S.

Strategy Shift & Growth

So you may be wondering, "If Smith & Wesson is so popular, why did they change their name from Smith & Wesson Holding Corp. to American Outdoor Brands Corp.?" Firearms are an extremely cyclical business. While there does exist a segment of the population that collects newly released models of firearms, much like Nike's Jordan fanatics, consumer firearm sales tend to follow volatile political and economic patterns. Sales tend to increase dramatically when the public fears increased gun regulation or the economy is in a down cycle and people feel the need to product their homes/assets. Due to the cycle nature of the firearm industry, management made the decision to expand into parallel but correlated niche markets of the outdoor sporting goods industry to make the business less cyclical for shareholders. As of January 2016, AOBC operates much like Berkshire Hathaway or Johnson & Johnson where it is nothing more than a holding company of excellent brands.

The decision to alter strategies was made by what I consider to be prudent and owner-minded management. In 2011 (AOBC's FY2012), James Debney was promoted to CEO of AOBC. Debney was the president of National Presto (NYSE:

NPK) from 2006-2009 and if you take a look at their financial statements, they have not seen the same revenue, earnings, or margin growth since he left. AOBC has seen significant growth and improvements in revenue, earnings, margins, etc. since he became CEO in 2011:

- Revenue (2011-2016): 16% CAGR

- Operating Cash Flow: 34%

- Free Cash Flow: 51%

- Net Income: 56%

- Book Value: 22%

- Shares Outstanding: -2.6%

- Gross Margin: 30.6% to 40.6%

- Operating Margin: 5.2% to 21.9%

AOBC grew firearm revenue from $328M to $600M from 2011 to 2016. However, the percentage of total revenue contributed by firearm sales dropped from 96% in 2011 to 83% in 2016. The other 17% came from strategic acquisitions into the firearm accessories and outdoor sporting goods markets.

Management

Warren Buffett & Charlie Munger have always held the belief that corporate management, especially the CEO, should first and foremost be an excellent allocator of capital. More often than not, when companies start depending on acquisitions for growth they make poor capital allocation decisions, acquiring at premiums and leveraging up the balance sheet. In the

FY2014 Annual Report under Strategy, management states that they are "focused on growth but only in areas that provide accepted return on invested capital." This statement had not been present in the five prior annual reports and after reading through the reports, it became evident to me that AOBC's management have been wisely allocating capital to grow the business and benefit shareholders. Here are examples since the CEO change:

- AOBC held the rights to produce and market Walther Firearms, maker of the famous PPK, products in the U.S. from 2002 to 2014. They ended the partnership because the manufacturing of lower margin Walther products was not as profitable as higher margin S&W products.

- Prior management acquired Universal Safety Products (renamed to Smith & Wesson Security Solutions), a perimeter security company, in 2009. Management discontinued and divested this business in 2012 due margin compression and lower revenue from constrained government budgets.

- Management acquired Battenfeld Technologies (NYSEMKT:BTI) in December of 2014 (FY2015) for $135.4M. Battenfeld had been growing revenues at 22% annually since 2008 and contributed $20.6M to AOBC's top line in FY2015. Due to being acquired with only 4 months left in the year, that equates to an adjusted premium of 2.2x sales, or 45% return on investment.

- DRP was acquired at the beginning of FY2015 for $23.8M and contributed $10.6M to revenue; another acquisition for 2.2x sales and 45% return on investment.

- In the fall of 2016 (FY2017), AOBC acquired Crimson Trace and Universal Survival Technologies (UST). Crimson Trace and UST had been growing revenues, compounded annually, at 10% and 49%, respectfully. FY2017 will be reported in June so the numbers are not available for these acquisitions yet. Based on this management's recent track record, I am confident that these were smart buys.

All of these acquisitions have been made with cash on-hand, current cash flow, and minimum debt. If debt was issued, the purchase price was low enough and cash flow strong enough that the acquisition was paid for within 12-18 months. Also, due to the structure of the holding company, AOBC is vertically integrating what they call the "distracting" parts of these companies, such as HR, Finance, etc. and retaining executive leadership, sales, marketing, and R&D.

Furthermore, management started a repurchase program and purchased $165M in shares between April 2012 and April 2015. These purchases were made in FY2013 & FY2014:

- 2.1M shares @ $9.53: P/E 8.1

- 7.5M shares @ $10.00: P/E 8.5

- 10.1M shares @ $11.32: P/E 7.6

They authorized another $50M for repurchases in June 2015 that expires in June 2017 but have not made any repurchases yet. The PE between June 2015 and Q4 2016 averaged above 15. Debney, personally, has recently been on a shopping spree buying shares. I am fairly certain that if management has been this prudent and insiders are buying, they are unloading that $50M right now to repurchase a little over 4% of shares outstanding.

Concerns

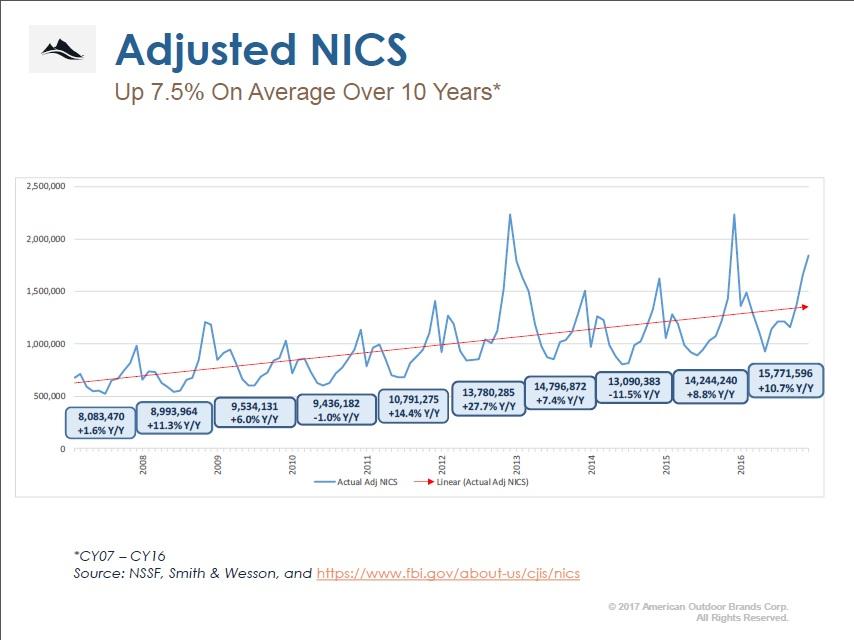

The biggest concern for shareholders at the moment is the forecasted decrease in

NICS background checks and softer firearms market due to the recent election and alleviating fears of heightened gun control by this administration. While this may be true in the short term, over the past 10 years, NICS background checks have grown at 7.5% annually. For short-term, swing trade investors, this is not what you want to hear and may be why 25% of the shares outstanding are being shorted. An opportunity may have presented itself for the 2-5+ year investors who are armed with the knowledge that the firearms market in the U.S. and NICS checks continue to grow at 4.6% and

7.5% annually, respectfully. This and management's efforts to diversify revenue to non-cyclical businesses presents an opportunity.

A second concern is management not making good capital allocation decisions moving forward. Based on their prior track record, I believe that they are a good bet although I will continue to monitor this closely.

Valuation

Qualitatively, I really like what I am seeing with top/bottom line growth and managements efforts to allocate capital effectively. Quantitatively, I need to figure out what the business is intrinsically worth based on a desired rate of return (or discount rate). When I evaluate intrinsic value and the growth of that value within a company, I like to look at Return on Incremental Invested Capital (ROIIC). There is a great

article by John Huber at Base Hitting on the background and specifics of ROIIC. In essence, I want to quantitatively understand how effectively management has been allocating capital and what percentage of capital is being allocated over a certain time frame in order to forecast capital allocation returns in the future. I use the below calculations:

- ROIIC: Change in earnings (or cash flow) / Change in capital invested; i.e. ROIIC = $78M ($131M) / $243M = 32.1% (53.9%)

- Reinvestment Rate: Capital Invested / Cumulative Earnings or Cash Flow; i.e. Reinvesment Rate = $243M / $328M ($510M) = 74% (47.6%)

- Intrinsic Growth: ROIIC x Reinvestment Rate; i.e. Intrinsic Growth = 32.1% (53.9%) x 74% (47.6%) = 23.7% (25.7%)

After comparing total capital invested and the reinvestment rate of that capital to the change in net income and operating cash flow, I calculated that the intrinsic value of the business has been growing at ~24% annually since 2012 (Debney's first full FY). This correlates closely with the 22% CAGR of book value and 27% RoRE (incorporates ~3% decline in outstanding shares).

If I apply a 20% growth rate (4% less than the 24% calculated) to Net Income & OCF and reduce outstanding shares by 3% annually, here is what I expect the business to be producing in 2022:

- Net Income: $94M (2016) to $234M (2022)

- OCF: $169M to $420M Shares Outstanding: 56M to 48M

I believe that AOBC could and should be trading at valuation multiples of 10x P/E and 6x P/CF, which is close to long term averages. This gives me a future price in 2022 between $48-$52/share, or a CAGR of 20%-22% from today's price of $19.50/share. Of course the growth rate or multiples could be lower moving forward but I expect that as AOBC continues to grow its core business, expand margins and revenue by acquiring strategic, higher margin business, and reducing share count when prices are attractive, we will see intrinsic growth rates similar to what we have seen in the past.

Conclusion

I believe that while the S&W brand is the beginning of a moat in itself for AOBC, the cyclical and discretionary nature of firearms does not allow this moat to grow unassisted. AOBC's management has shown in recent years that they are allocating capital wisely and getting good returns on said invested capital. If management continues to expand wisely into new growth markets while growing margins and revenue in firearms, we should see 15% CAGR at a minimum for the next 5 years.

Disclosure: I am/we are long AOBC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.